Unlocking the Economic Dividend of Resilience Investment

We often talk about resilience investment as a way to avoid tomorrow’s losses. That matters. But it’s only half the story.

Right now, with tight public budgets and a sluggish economy, we need to be clearer about what resilience investment delivers today: jobs, healthier communities, better environmental outcomes, and infrastructure that performs better day to day – not just during the next big event. Framed well, resilience stops being a “cost of risk” and becomes a practical form of economic stimulus and place-making.

Insurers are already signalling the direction of travel through risk-based pricing. They’re right to push for targeted investment that keeps cover available and affordable. The opportunity for our sector is to go one step further: build the business case around co-benefits and use it to unlock new funding models – including credible pathways for private-sector investment – alongside government and local government spend.

The challenge: a narrow view of value

Most resilience business cases focus exclusively on avoided losses – the cost of floods, slips, or coastal inundation that won’t happen if we invest now. This approach makes sense for insurance pricing, but it misses the broader economic picture.

When councils assess a flood protection scheme or a managed retreat programme, they’re typically measuring success against one question: “What losses will this prevent?” The problem is that this framing makes every resilience investment look like a defensive cost rather than a productive opportunity.

This narrow lens has three consequences. First, it undervalues projects that deliver immediate benefits – ecological restoration, improved amenity, or infrastructure that performs better under normal conditions. Second, it makes resilience investment politically harder to justify when budgets are tight. You’re asking ratepayers to pay now for something that might not happen for decades. Third, it leaves economic stimulus on the table – because we’re not quantifying or communicating the jobs, regional development, and business confidence that resilience projects generate.

A broader framework exists

More than a decade ago, the Global Facility for Disaster Reduction and Recovery (GFDRR) identified what they called the “triple dividend of resilience”:

- Avoided losses (first dividend) – the direct costs are prevented when a hazard event occurs

- Economic and development benefits (second dividend) – jobs, growth, and investment unlocked by reduced risk and uncertainty

- Social and environmental benefits (third dividend) – improved wellbeing, amenity, ecology, and community confidence

The second and third dividends matter because they accrue regardless of whether the hazard event happens. In our current economic context, that’s critical.

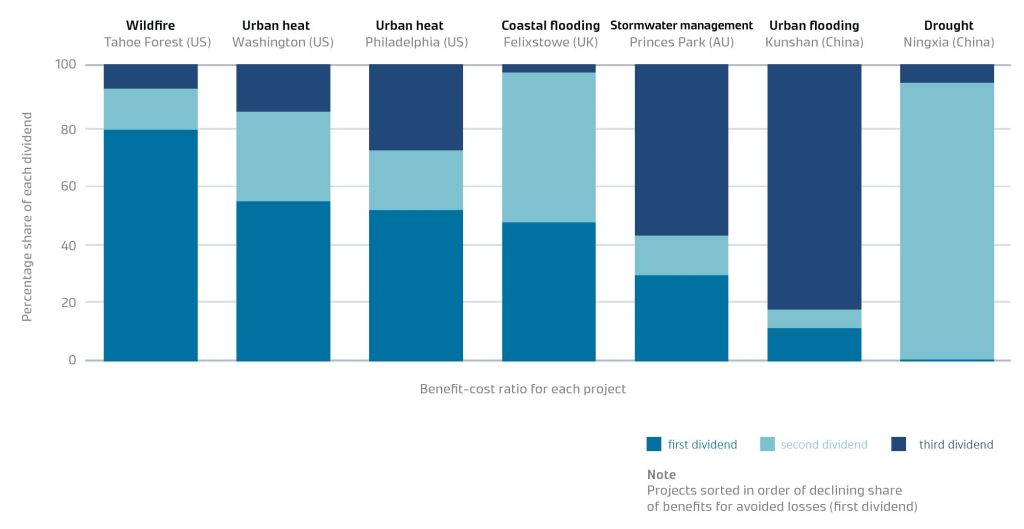

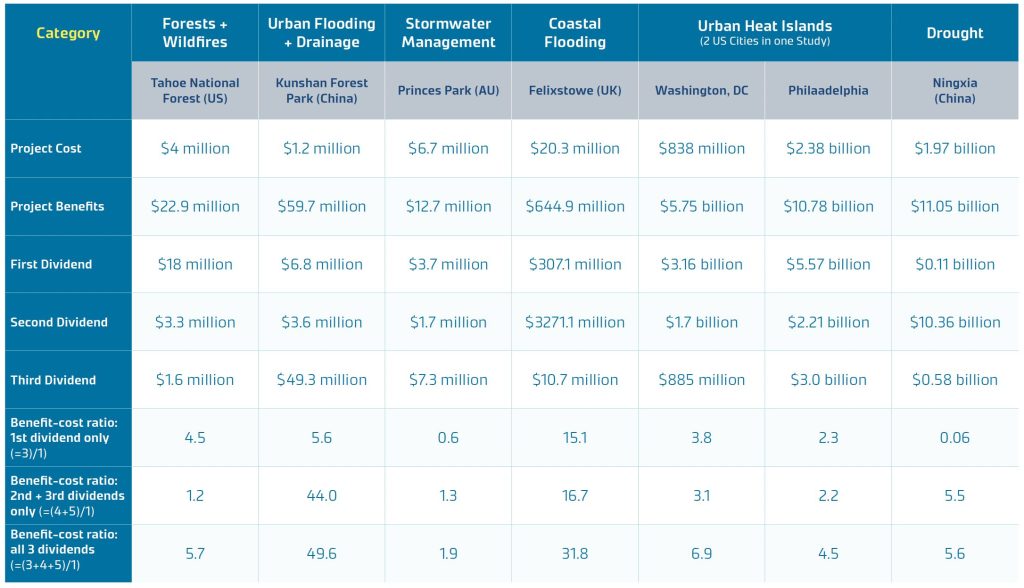

Each triple dividend as share of total project benefits

Overview of triple dividend case studies + breakdown of the dividends

A 2021 assessment of seven global case studies found that the second and third dividends exceeded the first in three cases. Projects most closely linked to water management – flood protection, stormwater systems, coastal adaptation – showed the greatest build-up of these broader benefits.

We believe councils and regional authorities should be making investment decisions based on all three dividends – not just avoided losses.

If you frame resilience purely as insurance against future risk, you’ll struggle to justify investment until the risk becomes urgent. By then, your options narrow, costs escalate, and you lose the opportunity to deliver co-benefits that matter to communities now.

Risk, volatility, and uncertainty are well-established suppressors of economic growth and investment. When natural hazard risks are well managed, households and businesses feel confident investing in productive assets rather than holding cash reserves for potential shocks. This drives job creation, modernisation, and regional economic stability.

New Zealand has historical proof of this. Between the 1930s and 1980s, we invested billions in flood protection infrastructure to safeguard productive land. Those assets now hold a combined capital and operational value of $3.6 billion and deliver $13 billion in benefits to New Zealand each year – a return multiple of 3.6 times the asset value.

The same economic logic applies to today’s adaptation and resilience challenges. The question is: how do we structure investment to capture all three dividends, especially when public funding is constrained?

Activating private investment: the beneficiary-pays principle

The funding challenge

While the case for investing more in resilience is clear, New Zealand’s fiscal reality is that this cannot be achieved solely through public-sector funding. Many councils face severe constraints as they approach debt-to-revenue limits and grapple with ratepayer affordability. Central government, with net core Crown debt approaching prudent limits, is focused on debt reduction as a percentage of GDP.

If the public sector cannot fund all necessary investments on its own, we need alternative models that enable private capital to participate.

Among the principles that guide adaptation finance – polluter-pays, public-pays, ability-to-pay, and beneficiary-pays – the beneficiary-pays principle offers particular potential. This principle holds that those who benefit from resilience investment should contribute to its cost.

Beneficiaries include property owners whose land values increase, developers who gain access to newly protected or intensified areas, businesses that benefit from reduced disruption, and insurers whose risk exposure decreases.

Value capture mechanisms – such as targeted rates, development contributions, and infrastructure levies, such as those enabled by the Infrastructure Funding and Financing Act – can channel some of this benefit back into funding the investment. Blended finance approaches use public or philanthropic capital to improve the risk-return profile for private investors, allowing private funds to participate in projects they would otherwise avoid.

Property-scale resilience

Alongside large-scale infrastructure and financing innovation, significant resilience gains can be achieved at the property level. Measures like flood-resistant materials, elevated services, and improved drainage all contribute.

Three enablers would accelerate property-scale action: better insurance recognition of resilience measures (e.g., through premium reductions), access to low-interest loans similar to sustainable financing and streamlined consent processes – provided property owners don’t create negative impacts for neighbours.

When combined with system-level investment, empowering individual property owners creates a more resilient community overall.

Almost 700,000 New Zealanders and over $135 billion in building value are exposed to river flooding. Another $12.5 billion is exposed to coastal flooding. The scale of investment needed is significant. The opportunity is to frame this not as a burden but as a catalyst – for jobs, for better places, and for regional economic confidence.

To apply this in your context, ask:

- Are we quantifying and communicating all three dividends in our resilience business cases—not just avoided losses, but economic stimulus and quality-of-life benefits?

- Who benefits from our proposed resilience investment, and have we explored whether beneficiary-pays mechanisms could unlock additional funding sources?

- Are we designing projects to deliver co-benefits that matter to communities now, rather than framing resilience purely as future protection?

Getting clarity on these questions early – ideally at the strategic planning stage – helps you build stronger investment cases, access broader funding, and deliver outcomes that communities value today.

References

- GFDRR (2015) The Triple Dividend of Resilience

- Tonkin + Taylor (2019) Hiding in plain sight. An overview of current practices, national benefits and future challenges of our flood protection, river control and land drainage schemes. Prepared for River Managers’ Special Interest Group

- Dr David Hall (2022): Adaptation finance: risks and opportunities for Aotearoa New Zealand

- NIWA (2019): New reports highlight flood risk under climate change | Earth Sciences New Zealand | NIWA

About the Authors

Jon Rix | Finance + Insurance Sector Lead – Principal Flood Risk Consultant | Tonkin + Taylor

Jon brings 20 years’ experience in urban drainage, flooding, integrated catchment planning, climate adaptation, risk assessment and asset management. Jon delivers customer-centred outcomes for public and private sector clients, combining technical expertise, leadership, and project delivery to support strong community, environmental, cultural, and economic outcomes across the built and natural environments.

James Russell | Finance + Insurance Sector Director – Geotechnical Engineer – Climate + Natural Hazards Consultant | Tonkin + Taylor

James has worked across the Geotechnical, Resilience, Water Resources and Civil groups, allowing him to develop a diverse range of skills. These include a broad understanding of the techniques used to model various natural hazards and a strong grounding in infrastructure. His key strengths include project management and delivery, natural hazard assessment – specialising in earthquakes and liquefaction, data analysis – focusing on spatial data, risk and loss modelling, climate risk assessment and adaptation planning.